3/6/2026

Shape Shifters S.A.S.

Portable Compliance Is Coming

Financial institutions spend enormous resources verifying customer identities and assessing compliance risk. Yet this process is largely repeated every time a person or business interacts with a new financial institution.

Each onboarding requires institutions to collect documents, verify identities, and conduct risk reviews, even when those steps have already been completed elsewhere under comparable regulatory standards.

This repetition creates operational inefficiencies across the financial system and introduces unnecessary friction for customers. For individuals and small businesses in particular, repeated compliance checks can become a barrier to accessing financial services.

International policy discussions increasingly recognize that digital identity and verifiable credentials can address this problem by enabling compliance information to move securely across institutions while maintaining regulatory safeguards.

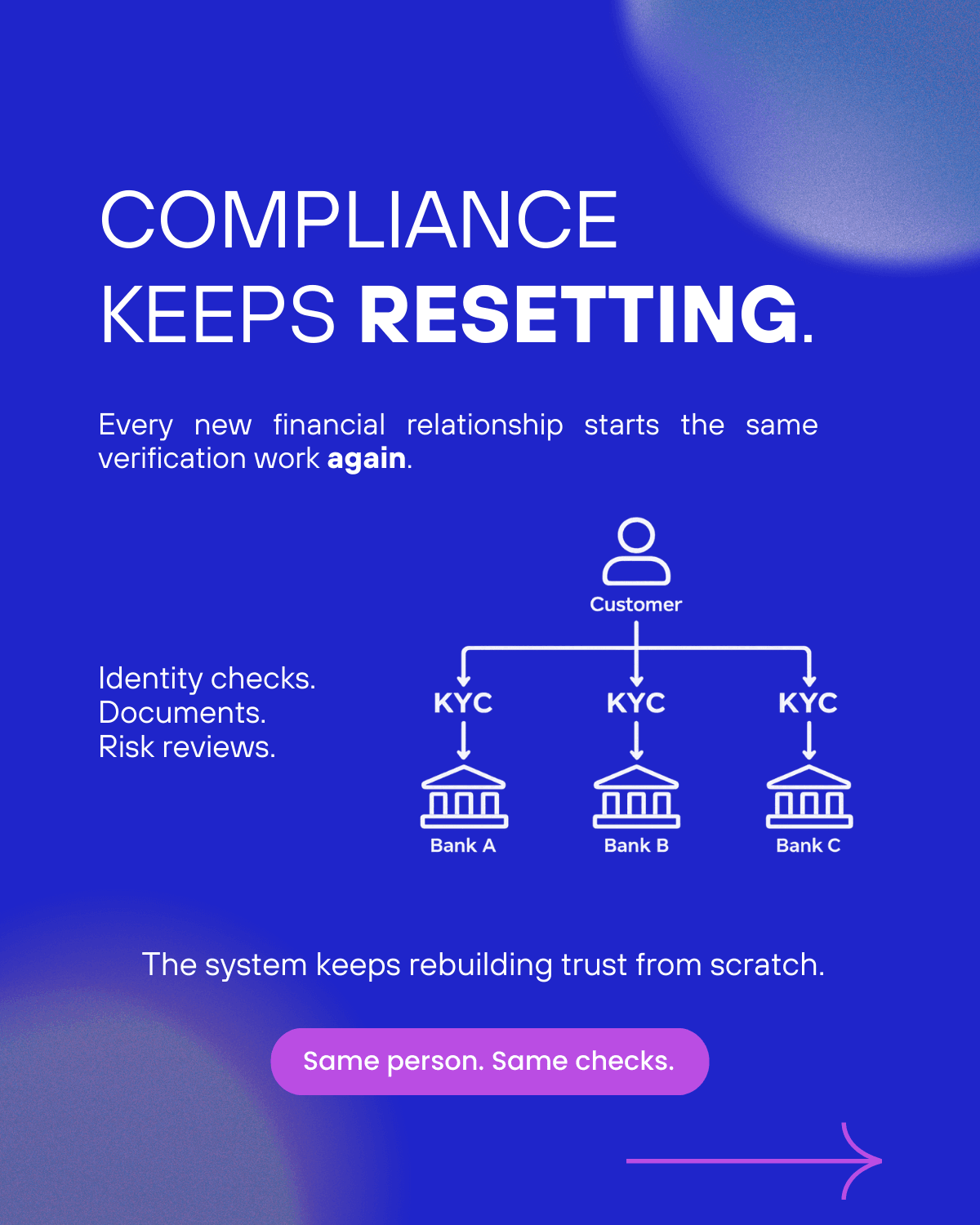

The Cost of Resetting Trust

Today’s compliance architecture treats customer due diligence as an institution-specific process. Each organization independently collects evidence, evaluates risk, and stores the results internally.

Even when multiple institutions operate under similar regulatory frameworks, verification results rarely travel between them. This leads to repeated documentation requests, duplicated reviews, and longer onboarding times.

For financial institutions, these processes generate significant compliance costs. For customers, they create friction that slows financial access and discourages participation in the formal financial system.

Global regulatory bodies such as the World Bank and the Financial Stability Board have emphasized that digital identity frameworks can reduce these redundancies while strengthening compliance controls.

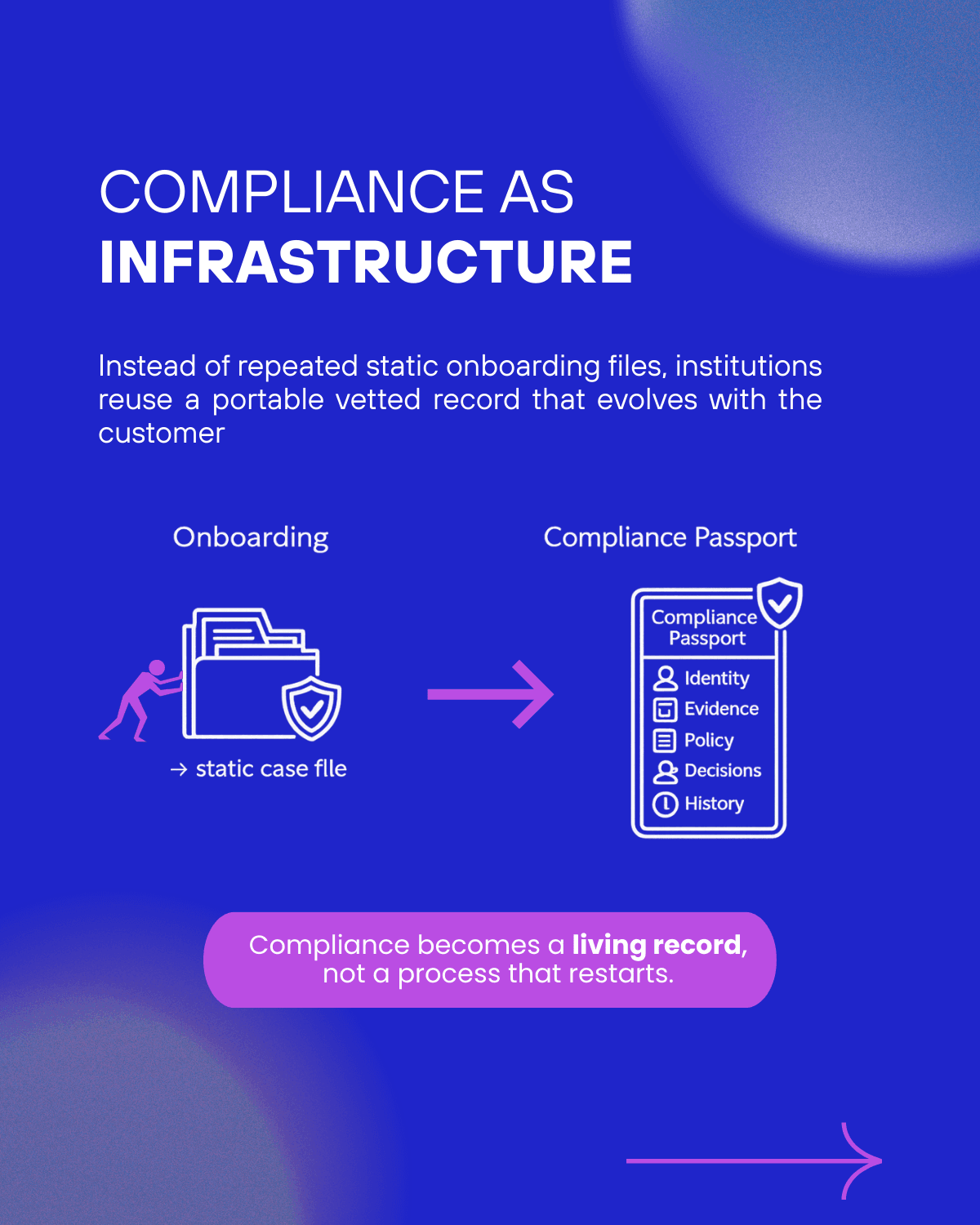

When Compliance Becomes Portable

A digital compliance passport introduces a different model. Instead of isolating compliance information within each institution, verified credentials can become portable and reusable across trusted participants in the financial ecosystem.

Under this model, identity verification and compliance assessments are represented through structured digital credentials that institutions can verify without necessarily storing or duplicating the underlying documentation.

This approach allows financial institutions to rely on previously verified information when appropriate, significantly reducing redundant onboarding work while preserving accountability.

Several global initiatives already demonstrate the viability of this approach. Digital identity programs in Europe, Australia, and other jurisdictions allow users to share verified identity attributes across services without exposing unnecessary personal data.

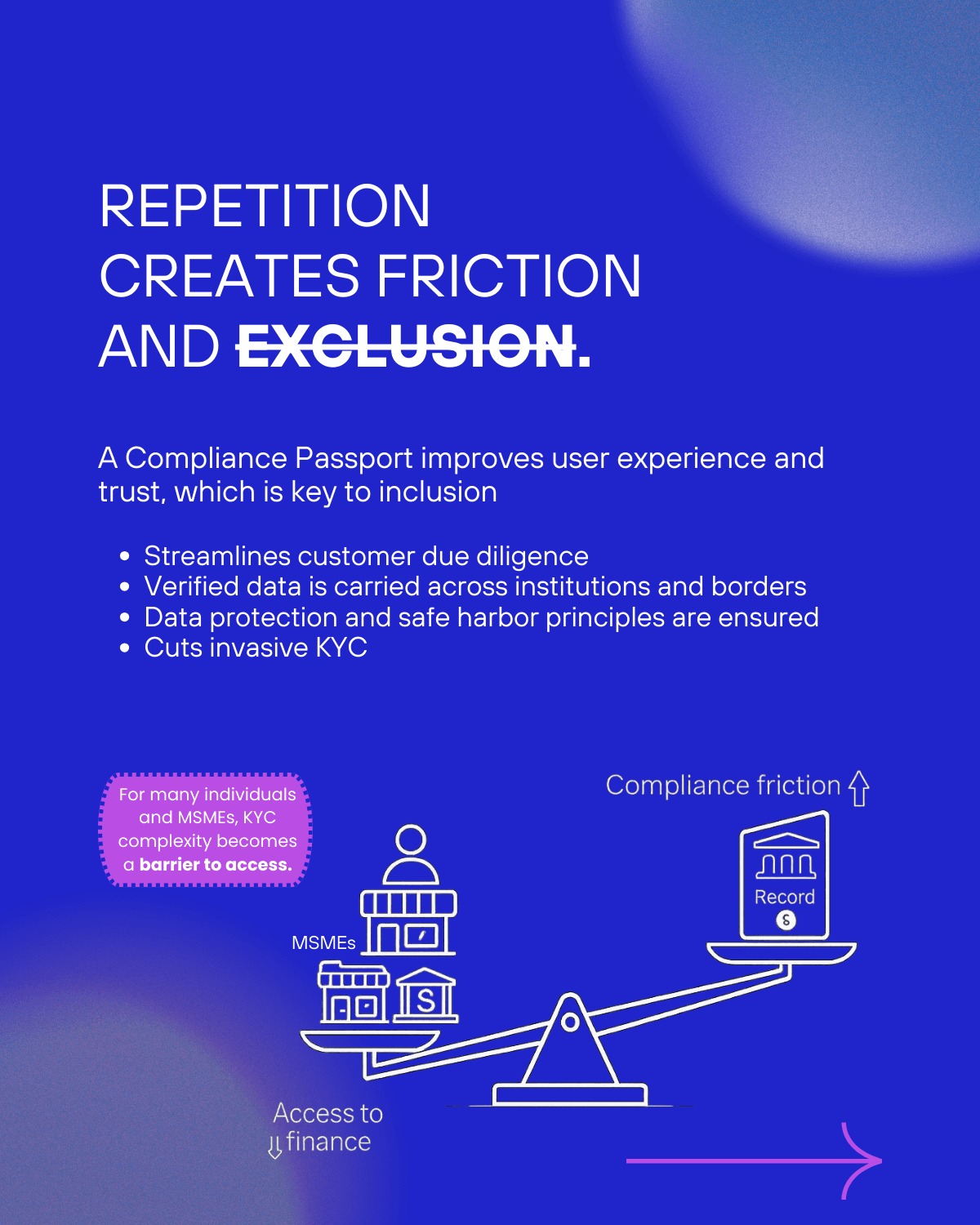

Why This Matters for Financial Inclusion

Repetitive compliance processes do more than slow down onboarding. They also limit financial access for populations that struggle to repeatedly meet documentation requirements.

Small businesses, informal workers, and individuals without extensive financial histories often face difficulties navigating repeated KYC procedures across institutions. When onboarding becomes too complex or intrusive, potential customers frequently abandon the process altogether.

Digital identity systems and portable compliance frameworks can help address these challenges by simplifying identity verification and enabling secure reuse of verified credentials.

International policy organizations have consistently highlighted digital identity infrastructure as a key tool for expanding financial inclusion while maintaining effective anti-money laundering safeguards.

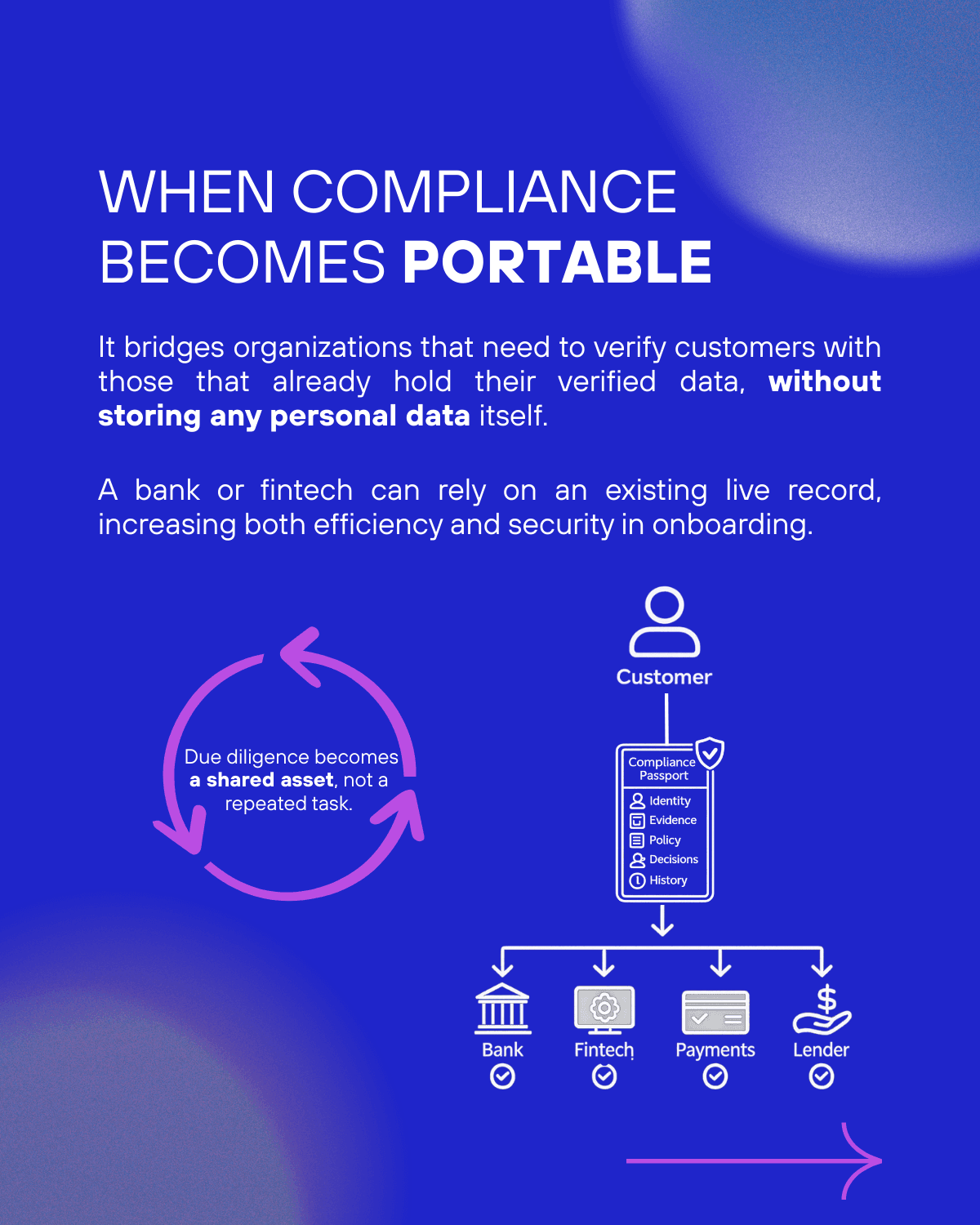

A Shared Trust Layer for Financial Systems

Portable compliance frameworks create a new type of infrastructure within the financial system.

Instead of treating compliance as isolated processes inside each institution, verification results can become part of a shared trust layer that connects banks, fintechs, payment networks, and lenders.

Institutions remain responsible for their own decisions, but they can rely on verified credentials issued within a trusted framework. This reduces duplication while preserving accountability and regulatory oversight.

Emerging regulatory initiatives suggest that this direction is gaining momentum. The European Union’s digital identity wallet, for example, aims to create interoperable identity credentials that can be recognized across both public and private services.

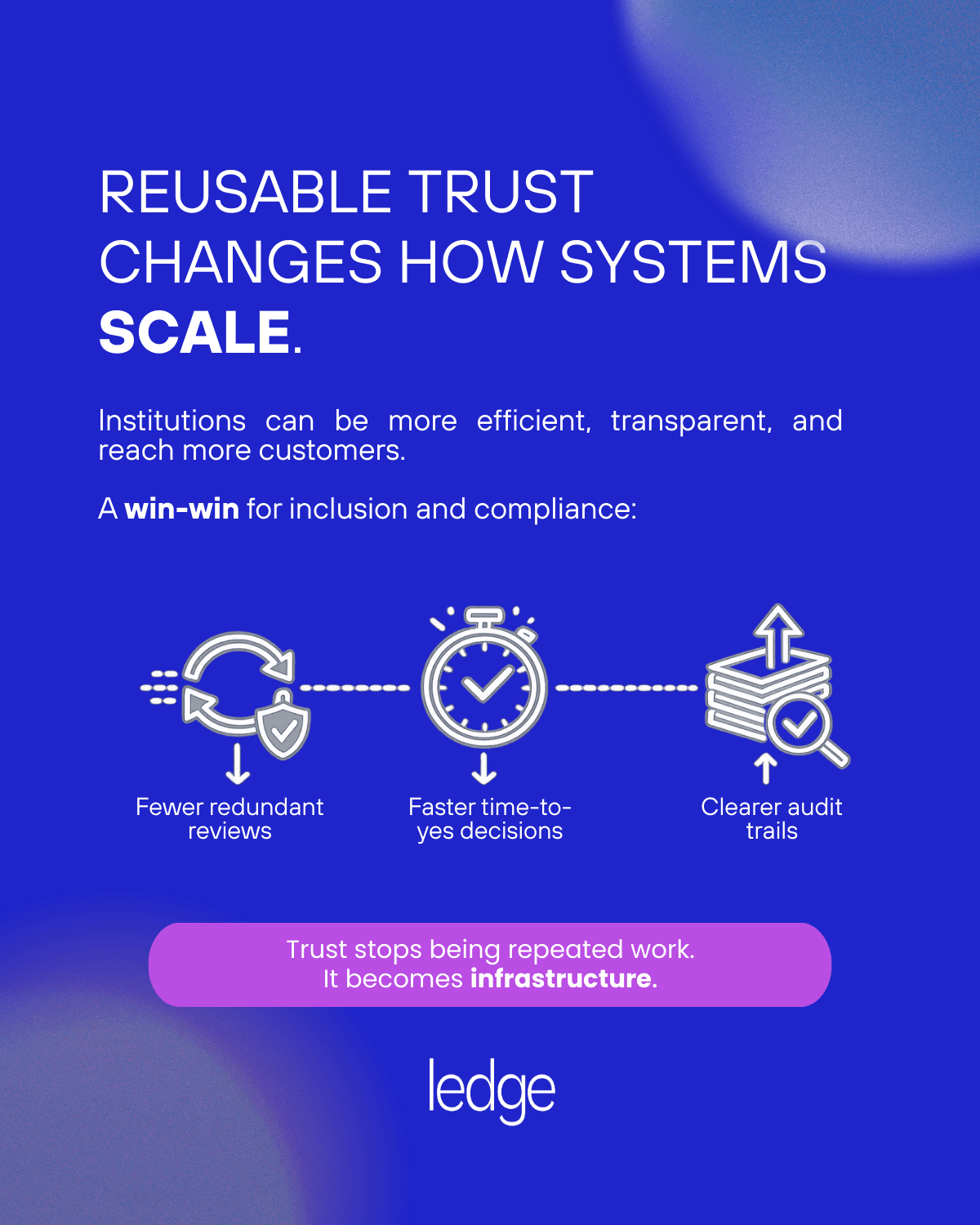

Scaling Trust Across Financial Networks

When compliance becomes reusable, the financial system becomes more efficient.

Institutions can onboard customers faster, reduce operational costs associated with repeated due diligence, and maintain clearer audit trails through structured digital records. Regulators benefit from improved transparency and more consistent compliance monitoring.

Most importantly, customers gain access to financial services with fewer barriers.

In this model, trust no longer needs to be reconstructed at every interaction. Instead, it becomes part of the underlying infrastructure that enables financial networks to scale.

References

Financial Stability Board, Digital ID for Financial Inclusion

FATF, Guidance on Digital Identity

World Bank, Digital Identity and Financial Access

BIS Innovation Hub, Streamlining Cross-Border Compliance

European Commission, European Digital Identity Framework